National

Petrochemical & Refiners Association

1899

L Street, NW, Suite 1000

Washington, DC

20036

LW-01-137

A

US MARKET SPACE ANALYSIS OF GTL LUBRICANTS

By

Thomas F. Glenn

President

Petroleum

Trends International, Inc.

Metuchen,

NJ

Presented

at the

NPRA

Lubricants & Waxes Meeting

November 8-9, 2001

Omni Houston Hotel

Houston,

TX

Publication

of this paper does not signify that the contents

necessarily reflect the opinions of the NPRA, its

officers, directors, members, or staff.

NPRA claims no copyright in this work.

Requests for authorization to quote or use the

contents should be addressed directly to the author(s)

ABSTRACT

Gas-to-liquid

(GTL) processing provides a means to convert natural gas

to such products as diesel fuel, jet fuel, naphtha, base

oil, wax, olefins, and alcohols. The products produced by

GTL are typically exceedingly clean. In addition, they

have very favorable manufacturing economics.

Lubricant

base oils produced by GTL processing are expected in the

market in the 2005/2006 timeframe. They are expected to

initially enter the market by competing with Group III and

IV in the synthetic and synthetic-blend engine oil market

space. To a lesser extent, GTL base oils will also compete

with Group II+ as a correction fluid for Group I in 10W-30

formulations, and as a workhorse against Group II+ in a

growing market for 5W-30. Rather than reducing the value

of GTL by moving down the quality continuum to Group I and

II base oils, GTL base oils are expected to reside in the

high-end market space of Group II+, III, and IV and be the

beneficiaries of demand being pushed into this market

space by more stringent specifications.

In

addition to GTL competing in the emerging low viscosity

passenger car motor oils markets, it will also penetrate

automotive driveline applications, premium diesel engine

oils, and high-end industrial lubricant applications over

the next five to eight years.

ACKNOWLEDGEMENTS

This

paper is based on primary research conducted by

PetroTrends professional staff over the last three months.

In addition, it includes information derived from such

secondary resources as the Internet, and other public

domain documentation. It is also supplemented by

information and insights provided by Nexant Chem Systems.

Nexant Chem Systems is a market research and consulting

firm. The firm recently completed a multiclient study

focusing on the manufacturing economics of GTL; Stranded Gas Utilization: Methane Refineries of the Future."

PetroTrends

would also like to acknowledge Syntroleum for sharing its

insights on some of the typical performance

characteristics for GTL base oils.

BACKGROUND

The

technology of converting gas to liquids (GTL), is based on

the chemical process known as Fischer-Tropsch (F‑T)

synthesis. The products produced by GTL include naphtha,

kerosene, jet and diesel fuels. In addition, GTL plants

also produce such specialty products as lubricant base

oils, waxes, olefins, and alcohols.

Interest

in GTL has grown rapidly over the last five years for

several reasons. First, it provides a means to monetize

significantly more of the world’s natural gas reserves.

These reserves are estimated at over 14,000 TCF and hold

the potential to produce an equivalent of several hundred

billion barrels of crude oil. According to a study on GTL

by Arthur D. Little, an estimated “900 TCF of gas

reserves are potentially suitable for monetization by GTL

technology.” A significant percentage of these reserves

are located in regions where there is little to no

domestic demand or too far from export markets to have

much economic value.

Beyond

the value of generating more equivalent crude, however,

GTL provides an economically attractive means to produce

fuels and specialty products far cleaner then those

derived from traditional crude oil processing. This is

particularly important in light of the increasingly

stringent diesel fuel regulations coming into play. In the

US, for example, the United States Environmental

Protection Agency (EPA) will mandate a maximum of 15 parts

per million (ppm) sulfur level in diesel fuel in 2006.

Even more restrictive regulations are expected in

Europe. In May of this year, the European Commission

proposed phasing in a 10 ppm limit on sulfur starting in

2005. Similar requirements are also on the horizon in

Japan and other countries. These and other sulfur limits

on the horizon will be a significant challenge for

refiners to meet when one considers that the average level

of sulfur in much of the diesel produced today is roughly

300 to 350 ppm.

Diesel

fuel produced by the GTL process is exceedingly clean. It

has no detectable levels of sulfur or aromatics. It also

has significantly higher cetane numbers than its crude oil

derived counterpart. Diesel produced by the GTL process

can be used directly as ultra high quality fuel, or as a

blend component to boost the performance of lower quality

traditional diesel fuel. Similarly, GTL processing also

produces high quality (e.g. low sulfur, low aromatic

content) kerosene, jet fuel, naphtha and a number of such

specialty products as olefins, waxes, lubricant base oils,

and others.

In

addition to producing very high quality, environmentally

desirable “synthetic fuels, or synfuels” and specialty

products, GTL is also attracting a high degree of interest

because it provides a means to eliminate flaring and/or

reinjecting natural gas. Flaring is considered an

environmental issue and technology that eliminates it has

value. Although somewhat a longer-term issue, GTL also

holds promise as a fuel source for fuel cells. Fuel cells

are expected to begin penetrating the internal combustion

(IC) engine market in roughly five years. The reformers

used in automotive fuel cell applications will have an

appetite for only the cleanest fuels, and GTL fuel can

offer the desired level of purity.

Driven

by the opportunity to monitize natural gas, and the other

issues mentioned, interest in GTL has climbed over the

last few years. Currently there are 13 announced GTL

projects in the world. Taken together they have the

potential to produce an estimated 870 thousand barrels a

day (TBD). The

most active regions in terms of number of plants are Qatar

and Australia; three plants have been announced for each.

Egypt is also expected to be a hotbed of GTL production

with two announced plants with a combined capacity

estimated at 145 TBD, as shown in Table 1.

|

Table

1

ANNOUNCED

GAS-TO-LIQUID PLANTS AS OF OCTOBER 2001

|

|

Location

|

Planned

capacity (TBD)

|

|

Qatar

|

290

|

|

Egypt

|

145

|

|

Australia

|

115

|

|

Argentina

|

75

|

|

Trinidad

|

75

|

|

Indonesia

|

70

|

|

Iran

|

70

|

|

Nigeria

|

30

|

|

Total

|

870

|

Although

much of the current interest in GTL is tied to monitizing

stranded gas to produce high quality diesel fuel, it has

also garnered interest due to its ability to generate high

quality specialty products, including lubricant base oil,

waxes, and olefins. In fact, there are two companies

currently using Fischer-Tropsch reactions to produce

‘synthetic” waxes.

Schümann Sasol operates a plant in South Africa

and Shell operates a plant in Bintulu Malaysia. The Shell

plant uses the Fischer-Tropsch reaction in the Shell

Middle Distillate Synthesis (SMDS) process to convert

long-chain paraffinic feed into wax and other specialty

products. Both the products produced by Shell and Schümann

Sasol have very high purity and sharp hydrocarbon

distributions. These products are typically hard waxes

with very high melting points (e.g. above 200°F)

Unlike

petroleum wax, which is a mix of iso- and normal paraffins,

F-T wax is pure normal paraffin in the C20 to C60+

range. The

characteristics of F-T waxes give them a significant

advantage over traditional petroleum waxes in such

high-melt applications as hot-melt adhesives, powdered

coatings, inks, textiles, color concentrates, and

plastics. In addition, F-T waxes are also advancing into

the phase change materials (PCM) market. This includes

such applications as heating systems, food transportation,

medical devices and therapies, and other applications

where the latent heat available from phase change can be

put to work. The global market in the high melt space is

roughly 80 to 90 million pounds, valued at roughly $50

million, or about 1% of the total global wax demand.

Although F-T waxes offer clear advantages in some

applications, in others they are disadvantaged due to

normal paraffin content and narrow hydrocarbon

distribution. This hydrocarbon profile does not currently

afford the same formulation and cut point flexibility

found in petroleum waxes and in a market as diverse and

diffuse as the wax business, formulation flexibility

offers a distinct advantage to wax suppliers.

Opportunities

in the wax market and how GTL waxes might compete in this

market space do weigh into the economics of building

plants. As a result, the outlook for GTL base oil is also

a function of the outlook for wax from these plants. This

is not to say that one could not justify the economics of

a GTL base oil plant without wax, but it does suggest that

the economics of a specialty GTL plant could be improved

if high-value wax were part of the product mix. As it does

relate to the outlook for GTL base oil production,

additional background on GTL wax and how its market space

is likely to develop follows.

GTL

wax. Most

of the wax in the market today is derived from base oil

production. Although certainly a valued product,

technically it is a byproduct of classic solvent refining

– solvent dewaxing base oil production. Unfortunately,

as a byproduct of base oil production, the future of the

petroleum wax business is not in its own hands. Instead,

it is in the hands of the lube base oil unit, and times

are changing.

Lubricant

base oil manufacturers are feeling pressure to incorporate

catalytic dewaxing technology to meet increasingly

stringent base oil performance requirements. The catalytic

dewaxing process does not yield wax. Instead, the wax

molecules are cracked and isomerized into base oil, fuels,

and other fractions. The impact of this shift has been felt greatest in the North

American market. In

the last five years, a major grassroots base oil plant was

built (Excel Paralubes) using catalytic dewaxing and three

others replaced existing solvent dewaxing technology with

catalytic dewaxing. Others

are expected to follow.

In addition, Petro-Canada added ISODEWAXING

capacity to its plant in late 1996.

In addition to declines in wax supply as a result

of conversions from solvent dewaxing to catalytic dewaxing,

supply in North America has been further eroded by the

exits of several smaller base oil producers.

These exits took wax with them.

As

discussed, how the market space for GTL base oils develops

will, in part, be influenced by the business opportunities

associated with the wax market and how these opportunities

might compete with other interests. GTL projects are

considered to have the potential to greatly increase wax

supply because roughly 50% of the yield from the syngas

reactor is wax. The economics of world scale GTL plants,

however, will

be driven by demand for low sulfur diesel fuel, not wax

and other specialty products.

Beyond

the big picture economic realities of a world scale GTL

plant, a number of the major oil companies (those with the

resources to build a world scale GTL plant) would also

have to look across their businesses before heading into

the wax market. Many of the majors still produce wax from

solvent dewaxing. These companies will likely face the prospects of

cannibalizing their existing wax business should they

decide to market wax from a GTL plant. For some, this may

prove to be a losing proposition where every pound of wax

moved into the market from the GTL plant displaces a pound

of wax they have already placed in the market and produced

from its solvent dewaxing unit.

The

next likely new entrant into the F-T wax supply pool would

be a specialty products supplier with its eyes on base

oils, wax and other specialty GTL products. This would

likely be a producer with no ties to a conventional

solvent-refining/ solvent-dewaxing lube base oil plant.

Such a player would not have to consider the issue

of cannibalization and could develop the high-melt wax

market competing aggressively in an effort to grab market

share. Although a specialty products GTL player could

potentially do this, the value of this effort is

questionable since the high-melt point wax market is

fairly well balanced. It is also important to note that a

new entrant into the F-T wax market in the high-melt

market space would be competing with entrenched suppliers.

They would also be competing with PE wax suppliers. PE wax

is already a formidable competitor with F-T in the

high-melt market space.

A

new F-T wax producer could also decide to target the large

market spaces occupied by mid- and low- melts petroleum

waxes. This, however, is not a straightforward process.

F-T wax suppliers would likely find it necessary to

fractionate the wax because the C20 to C60

range of normal paraffins is too wide for most

applications. They

may also find it necessary in many applications to blend

F-T wax with petroleum waxes in order to match performance

requirements with existing expectations. Even with the

cost burden of fractionation and blending, the cost

structure for F-T wax could prove an advantage.

In assessing the magnitude of this advantage,

however, one would have to remain grounded in the fact

that a decision to compete in this market space is a

decision to compete with a large volume of byproduct

coming from lubricant base oil production.

In

summary, this means that the primary driver for GTL plants

today is high-quality, environmentally friendly diesel

fuel, not lubricant base oils, waxes, and other specialty

products. The catalysts used in a plant designed to

produce GTL fuel and the alpha value of its products do

not readily lend themselves to base oil production.

BASE OIL MARKET SPACE DEVELOPMENT

Few

question if the market for GTL base oils will develop. The

primary questions asked today are when, where and how will

it develop, and who will develop it first. In addition,

there is a good deal of interest in the economics of these

plants. Insight into these and other questions starts with

an understanding of what GTL base oils are and what level

of performance they offer.

GTL

base oils are products synthesized by a Fischer-Tropsch

reaction. These base oils have no detectable levels of

sulfur, nitrogen, or aromatics, and they are water white.

They have a very narrow hydrocarbon distribution and

excellent oxidation stability characteristics. In

addition, the lower viscosity products (e.g. less than

4cSt) are typically biodegradable. GTL

base oils with viscosity grades used in automotive engine

oil applications (4.0 to 9.0 cSt) are expected to have a

Viscosity Index in the range of 140 to 155. By comparison,

PAO has a VI of 120 to 138 for the same viscosity range.

Another

very important attribute of GTL base oils and one that

will shape its place in the market is its volatility. GTL

base oils reportedly have NOACK volatilities significantly

lower than API Group I, II/II+ and III base oils. A 4 cSt

product, for example, is reported to have a NOACK

volatility several percentage points below 10, as compared

to a typical Group III with a NOACK in the low- to mid-

teens. These performance attributes position GTL base oils

well to compete with PAO and Group II+ and III in the

automotive lubricants market space. It also suggests that

the greatest value for GTL base oils will be realized in

the automotive lubricant viscosity grade ranges of 2 cSt

to roughly 10 cSt and that alpha values for specialty GTL

product producers will likely optimize on these grades.

GTL

base oils also have excellent low temperature properties.

In fact, they appear to be only slightly

disadvantaged when compared to PAO’s cold crank

viscosities. The

pour point of GTL base oils is, however, much closer to

that of a Group II/III than it is to a PAO.

This can be addressed by the use of pour point

depressant and GTL base oils are reported to have

excellent responsiveness to methacrylate -based pour point

depressants.

In

addition to high quality, GTL base oils also have very

favorable manufacturing economics. According to a

multiclient study recently completed by Nextant Chem

Systems, the manufacturing costs for GTL delivered in the

US market are comparable with that of Group I, II, and

II+. Even more importantly, ChemSystems' analysis reveals

that the economics for GTL are more favorable than that of

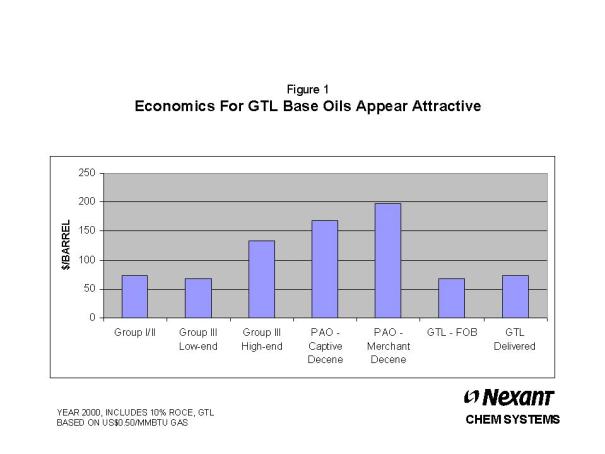

high VI Group III, as shown in Figure 1.

Considering

the manufacturing cost position of GTL base oils and its

performance characteristics, a starting point to begin

modeling market space development for GTL base oils is one

that looks at how the market space for API Group II and

III developed. These products also entered the market as

high performance base oils with attractive manufacturing

economics. An analysis of how the market space for Group

II and III base oils developed is provided as a backdrop

for how the market space for GTL base oils might also

develop.

Group

II and III base oils.

Group II and III base oils are product definitions that have

emerged over the last decade. The American Petroleum

Institute (API) developed the API base oil group

categories in an effort to differentiate the various

levels of base oils quality in the marketplace. In

addition to placing polyalphaolefin (PAO) in a class of

its own (GROUP IV). The system established three groups of

paraffinic base oils. These groups were based on

saturates, sulfur, and viscosity index (VI), as shown in

Table 2.

Table

2

American

Petroleum Institute Paraffinic Basestock Groups

|

|

|

Requirements

|

|

API

Group

|

Sulfur,

% wt.

|

Saturates,

% wt.

|

Viscosity

index

|

|

I

|

>

0.03 and/or

|

<

90

|

80

- 119

|

|

II

|

£

0.03 and

|

³

90

|

80

- 119

|

|

III

|

£

0.03 and

|

³

90

|

³

120

|

|

IV – a

|

-

|

-

|

-

|

|

V – b

|

-

|

-

|

-

|

|

a- Includes

polyalphaolefin (PAO).

b- Includes esters and other base oils not

included in API Groups I through IV.

|

Group

II and III base oils are generally considered superior to

Group I because they have a lower aromatic content and

higher viscosity index. Aromatic fractions tend to be more

unstable than saturated hydrocarbons, and as a result,

Group II base oils have superior thermal stability and

resistance to oxidation over Group I. In addition, as you

move up the continuum from Group II to III, you move from

base oils with a minimum VI of 95 to Group III base oils

with minimum VI over 120. This higher VI, together with

aromaticity and other issues, makes Group III base oils an

ideal blend stock to meet the more stringent volatility

requirements in passenger car motor oil. In addition, it

gives these base oils an advantage in heavy-duty motor

oil, and ATF.

Although

the API Group classifications do provide clear guidelines

to differentiate conventional and unconventional base

oils, it is important to consider the differences between

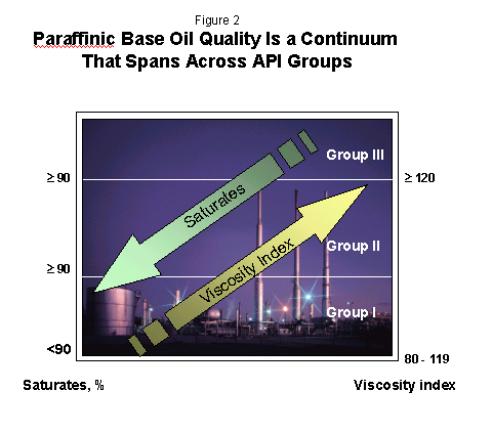

API Groups as a quality continuum based primarily on

saturates and VI, as shown in Figure 2.

The

importance of this continuum gave rise to the “Group

II+” designation. Although Group II+ is not an official

API definition; it emerged out of the need to describe

base oils with a meaningfully higher viscosity index than

the 100 than is typical of most Group II base oils. Group

II+ base oils typically have VI in the range of 108 to

115. These base oils offer performance advantages over

Group II in some passenger car motor oil applications,

specifically related to balancing volatility with low

temperature viscometrics.

Where

GTL base oils will fit in the API base classification

system has yet to be determined. Based on some of the

performance data currently being developed, however, it is

believed that GTL base oils would likely be handled in one

of three ways. One possibility is that another API group

will be established to accommodate it. Another possibility

is that it will simply fall into a Group III designation

because it does, in fact, meet the criteria for a Group

III. Another possibility is that GTL base oils will follow

the path of Group II+. This is likely to result in a

market-place designation of Group III+.

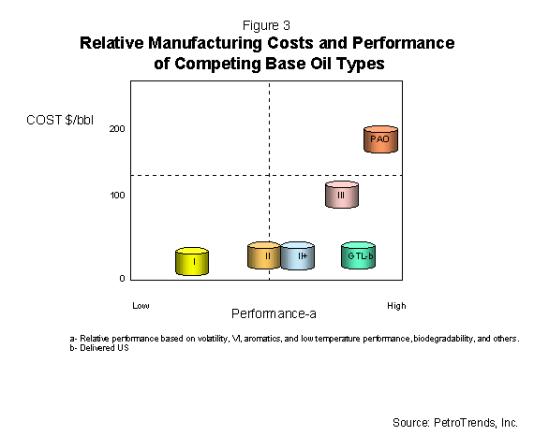

As shown in Figure 3, the performance of GTL is

considered nearly equal to Group III, however, it could

enjoy significantly lower manufacturing costs. The cost

and performance of GTL base oils suggest it will likely

track a market space development path similar to that of

III, and to a lesser extent, Group II+.

The

market space for Group II+ and Group III was developed on

several fronts, including:

- Direct

competition with PAO

- Low

volatility base oil solution for 5W-xx engine oils

- Blend

stock/correction fluid for other base oils

How the market

space for Group III and II+ developed in each of these

areas and how GTL market development might follow it is

discussed below:

Direct

competition with PAO.

Group III base oils are typically produced by incorporating

isomerization of wax fractions from the base oil into the

overall process. The isomerization process changes the

geometry of wax molecules to structures with acceptable

low temperature performance characteristics (they don’t

form wax and solidify at cold temperatures). In addition,

the isomerization of wax can significantly boost the VI of

the base oil. In fact, if run under more severe conditions

the VI of a paraffinic base oil can be pushed up to a

level that parallels that of PAO. Pushing VI up does,

however, come at the expense of yield. The high VI,

together with very low aromatic content of Group III, put

it in an excellent position to compete with PAO, and that

is exactly what it did when it entered the market.

PAO

had enjoyed a nearly unrivaled position as the

“synthetic” base oil of choice in automotive and

industrial lubricant applications.

It captured an estimated 2% of the total lubricants

market. Although PAO offered excellent oxidation stability

and unparalleled low temperature performance it had a

weakness that Group III exploited. Its weakness was

manufacturing cost. The cost to produce PAO was fairly

well studied and many were aware that the minimum costs to

produce PAO were significantly higher than that to produce

Group III. It was also well known that although Group III

could beat PAO on a cost basis, PAO still had the

virtually exclusive right to bear the valued

“synthetic” label, and PAO could far outperform Group

III in a cold crank simulator (CCS).

This advantage, however, virtually vanished

overnight when Castrol replaced PAO in its synthetic

engine oil formulation with extra high VI paraffinic base

oil. This represented a significant cost saving in the

formulation. It also resulted in a challenge from Mobil

regarding the use of the term “synthetic” by Castrol.

The challenge was brought to the National Advertising

Division (NAD) of the Council of Better Business Bureaus (CBBB).

On April 5, 1999 the NAD announced that Castrol North

America could continue to advertise its product as

“synthetic” motor oil even though Group III was being

used. Group III now had the right to wear the

“synthetic” lubricants label. Many lubricant

manufacturers switched from PAO to Group III shortly after

this ruling was announced to take advantage of the reduced

cost of the “synthetic” base oil.

In

addition to market opportunities as a replacement for PAO

in automotive applications, Group III has and will

continue to displace PAO in some industrial lubricant

applications. Its leverage in this space is, however,

weaker than it is in automotive engine oils. The

automotive engine oil segment ascribes high value to the

term “synthetic.” The industrial segment places far

less value on the term “synthetic” and much more value

on the performance advantages they offer. Although the

oxidation stability of Group III is similar to PAO, PAO

significantly outperforms Group III in low temperature

applications. As a result, market share capture by Group

III in the industrial lubricants space has come much more

slowly than in the automotive segment.

GTL

base oils have an opportunity similar to the one Group III

capitalized on in the PAO market space. The primary

difference, however, is that it will now be competing with

both PAO and Group III. Group III only had PAO to contend

with.

The

challenge for GTL in this market space, specifically in

synthetic and synthetic-blend automotive applications,

will be cost. Formulators switched from PAO to Group III

in automotive engine oils due to the cost savings one

could enjoy by blending with Group III. Any switch from

Group III to GTL would either have to represent a

relatively significant cost savings, and/or measurable

boost in performance. The performance advantages of GTL

over Group III will likely be found on several fronts. On

one front, GTL will promote the superiority of its

volatility over that of Group III. It is believed that GTL

will also use additive responsiveness and total

formulation costs as a tool to capture market share from

Group III and PAO. GTL

base oils may also provide “environmentally friendly”

solutions to the industrial lubricants market due to its

biodegradability and its absence of sulfur and aromatics.

Base

oil solution for low volatility in passenger car motor oil.

In addition to going head to head with Group III

and PAO in the high performance segment of the automotive

lubricants business, GTL is expected to compete with

Groups II+ and III with a model similar to the one used by

Group II, II+ and III to capture market share from Group I

in passenger car motor oil. It did so by responding to OEM

interests in fuel economy and the fact that the use of

lower viscosity engine oils can improve fuel economy. The

use of lower viscosity engine oils (e.g. 5W-30) did not,

however, come without concerns. In addition to the

market’s reluctance to embrace lower viscosity engine

oil grades, technical hurdles existed in regard to the

ability of the engine oil to stay in grade during use.

Engine oil can thicken and come out of grade when

subjected to the high operating temperatures in an engine

due to the light end boiling off. This meant that although

engine oil would yield desirable fuel economy performance

on an engine test stand, it did not necessarily reflect

what was actually delivered in service once the oil is

exposed to heat and aged in operation. In an effort to

address this issue, the International Lubricant

Standardization and Approval Committee (ILSAC) introduced

volatility into its GF-2 standard in the mid-1990s.

The

first iteration of GF-2 included a comparatively stringent

specification for volatility in multigrade passenger car

motor oil. It was tough, and the volatility of many of the

base oils on the market at that time did not offer the

performance necessary to meet GF-2. Base oil manufacturers

had several alternatives. One option was to narrow the

cuts in an effort to compress the hydrocarbon distribution

in the base oils. This solution was considered relatively

costly because, although it would reduce volatility by

effectively cutting off light ends, it also cut off longer

chained hydrocarbons at the other end of the distillation

curve. This approach placed a significant penalty on

yields and as a result, was costly. Another option that

could have been used to meet the first iteration of GF-2

was to blend conventional paraffinic base oil with

polyalphaolefin (PAO). This too, was considered a costly

solution because PAO was over four times the price of

conventional base oil. A third option was to work with

ILSAC and other industry stakeholders in an effort to

relax the specifications for volatility in GF-2 and give

the industry more time to prepare. The base oil industry

argued that it was not ready for such a restrictive

specification. Agreement

was reached to relax the volatility specification for GF-2

and most base oil manufacturers were then in a position to

meet the requirements.

Most

engine oils on the market at that time did come in under

the wire for the final version of GF-2. The process,

however, sent a clear message to the industry that

volatility would be revisited in the next passenger car

motor oil specification (GF-3), and that something other

than “conventional” base oil would likely be required

in the near future for those interested in competing in

the automotive lubricants business.

Although

most of the base oil in the US market was

“conventional” when GF-2 emerged, there was one

exception; Chevron. Chevron’s

Richmond plant operates with manufacturing schemes based

on hydrocraking and wax isomerization, specifically

Chevron’s ISODEWAXINGÔ

technology. Rather than removing impurities with solvents

and hydrotreating, this process uses a hydrocracking

process with special catalysts to literally break the

bonds of aromatics and saturate the remains of these and

other constituents in a high temperature, high-pressure

atmosphere that is rich in hydrogen. Unlike “conventional” solvent refining where the aromatic

content of the base oil is roughly 10%, hydrocracking

typically reduces the aromatic content of paraffnic base

oils to less than 1%. In addition, it typically produces a more refined cut in

terms of hydrocarbon distribution. These attributes, with

the catalytic dewaxing process that increases viscosity

index, resulted in base oils that could meet the more

stringent volatility requirements initially proposed in

GF-2 and beyond.

Interestingly,

although Group II base oils have been in the North

American market for close to 15 years and demonstrate

superior performance capabilities, they didn’t receive

much attention until about the last seven years. The primary reason was limited supply. As discussed, there

were only two producers in North America when GF-2 emerged

– Chevron and later Petro-Canada.

This changed, however, when Excel Paralubes (a

joint venture between Pennzoil and Conoco) built a

grassroots Group II plant that came on stream in 1997. The

Excel plant increased supply of Group II by nearly 20 TBD.

This additional supply gave Group II the critical mass

necessary to help convince automotive OEMs that the

lubricants industry now had the technology in place

required to meet more stringent specifications around

volatility. The new specification represented a step

change in PCMO volatility, as shown below in GF-3.

Table 3

NOACK Volatility

|

|

NOACK

Volatility (a)

|

|

PASSENGER

CAR MOTOR OIL GRADE

|

GF-1

|

GF-2

|

GF-3

|

|

0W‑

and 5W‑ multiviscosity grades

|

25

|

22

|

15

|

|

All

other multivisosity grades

|

20

|

22

|

15

|

|

NOTE:

(a) D-5800-99 standard test method for evaporation loss

of lubricating oils by the NOACK method.

|

This

specification would clearly favor the use of Group II and

pull through demand based on technical need. In fact, for

some grades, the specifications virtually required the use

of Group II and II+.

In addition, Group II was also showing promise as

value-added base oil in heavy-duty motor oil applications

and ATF. This too resulted in pull-through demand.

As

discussed later in this paper, GTL base oils likely will

be the beneficiaries of the momentum in pull through

demand established by Groups II, II+, and III in

automotive engine oil applications.

BLEND

STOCK/CORRECTION FLUID FOR OTHER BASE OILS

Although

base oil manufacturing is clearly shifting from Group I to

Group II in the US and Canada, Group I base oils are

expected to remain an important part of the supply pool.

These base oils are favored as the low cost workhorses for

a wide range of price sensitive industrial lubricant

applications. Some

lubricant blenders use Group I because they have captive

supply, others use it because it aligns well with their

product portfolios. In many cases, blenders heavily

reliant on Group I base oils will find it necessary to

bring in such high quality base oils as Groups II+, III,

and IV as a means to enhance the performance of the

workhorse Group I. An example of how a blender could use a

Group II+ to enhance the performance of a Group I can be

seen in a 10W-30 PCMO formulation. Although there are many

ways to meet the volatility requirements for GF-3 in a

10W-30, an economical option is to blend with roughly 70%

Group I base oil, 10% Group II+, and additives.

GTL

base oils are expected to compete with Group II+, III, and

IV as a blend stock to enhance the performance of Group I

base oils. Its ability to displace these competing stocks

is expected to be based primarily on performance and its

impact on total formulation costs.

GTL

BASE OIL MARKET SPACE DEVELOPMENT

GTL

base oils are positioned to track the footsteps already

established by Group II and II+ as the workhorse in some

multigrade engine oils and as a correction fluid in

others. The challenge for GTL base oils in the US,

however, will be the relatively sluggish market

penetration of 5W-30. In addition, Group II and II+ base

oils have already established themselves as the solution

for 5W- and 10W-30 engine oils. This means that additives

are well on their way to being optimized, blenders are

comfortable working with these stocks, and product

development costs have been invested.

Rather

than potentially giving away value by competing with

Groups I and II base oil in the 10W-30 PCMO market and

others, a more likely scenario is one that allows GTL to

maintain its value by waiting for the direction of

specifications to mature the market into the market space

currently occupied by Group III and IV, and to a lesser

extent Group II+. The direction of specification has

already moved a significant volume of base oil demand out

of the Group I space and into the Group II and II+ space

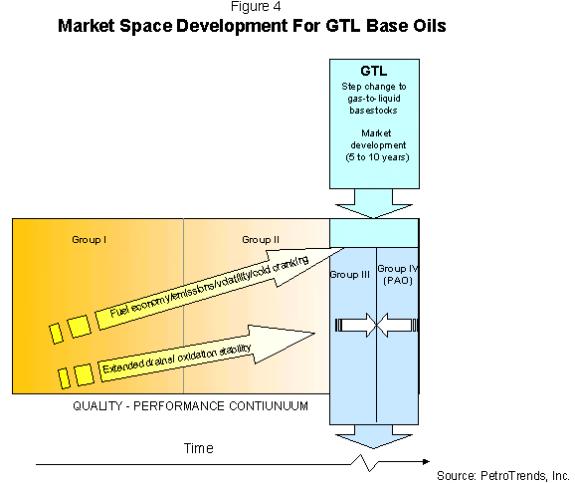

in the US market. Future

specifications will continue to push demand through the

Group II and II+ space into the space occupied by Group

III, Group IV and GTL, as shown in Figure 4.

The

challenge for GTL in this approach, however, is that the

market will take time to evolve into its space. This

evolution will be tied in a large way to market acceptance

of 5W- and 0W-xx engine oils.

The most significant pull-through demand for GTL

base oils in PCMO will, however, likely be tied to 0W-xx.

Meeting the volatility requirements in this grades is

expected to be attainable only with PAO and likely GTL.

Although the low temperature performance of GTL base oils

could be an issue, data exist to suggest that this issue

can be overcome by GTL’s favorable responsiveness to

additives. It is also important to consider, however, that

even with OEMs promoting the use of 0W-xx, consumers have

the final say. If market acceptance of 5W-30 is any

indication, consumers are slow to accept lower viscosity

grades even when OEMs recommend them.

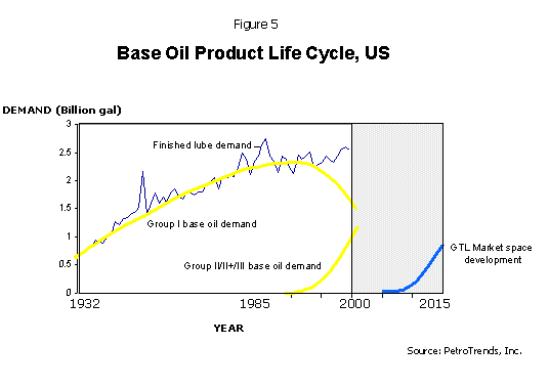

What

this means is that GTL will not likely be a significant

demand event in the US for at least the next eight to ten

years. From a product life-cycle perspective, we will

likely see GTL entering the supply pool in the 2005/2006

timeframe. If one uses the GTL plant completion schedules

currently tabled, the supply build model of Group II/II+

and III, and the grade switching rates of 5W-30 as a guide

to model with, the introduction phase of the GTL life

cycle will likely begin in 2005 and take about five years

before it advances into the growth phase, as shown in Figure 5.

Initially it will do so at the expense of Group III and IV

base oils by capturing market share in the synthetic and

synthetic-blend automotive lubricant market space. It will

also penetrate the ATF and automotive driveline market

space at the same time. Market acceptance of GTL is,

however, expected to be modest during this introductory

phase of its life cycle due to a limited number of

suppliers.

GTL

is expected to transition into a growth phase by capturing

demand away from Group II, II+, III, and IV as demand for

5W- and 0W-xx PCMO increases. As additional supply comes

on line it will give OEMs and blenders the assurances they

need that supply lines are adequate and secure. This will

catalyze growth-phase demand by moving it into a

push-demand scenario similar to that currently occurring

with Group II base oils. Push marketing will drive up

demand for GTL in heavy-duty engine oil and industrial

high performance industrial applications.

GTL

is also expected to capture significant market share of

the automotive driveline segments over this same period

due to fill-for-life initiatives.

It

is also important to consider that although GTL may not be

a significant event in the US over the next eight years,

it will enjoy more aggressive growth in Europe and Asia.

The lubricants market in Europe is more mature than that

in the US and market acceptance of 5W- and 0W-xx is

further along.

CONCLUSION

Although

the primary focus of gas-to-liquid (GTL) technology is

currently on opportunities in diesel fuels, base oils

derived from this technology could also be in place by

2005. Base oils produced by GTL processing are expected to

deliver quality superior to Group III and at very

competitive costs.

Base

oils produced by GTL processing are expected to initially

enter the lubricants market by competing with Group III

and IV in the synthetic and synthetic-blend engine oil

market space. They will compete with these base oils

primarily on performance and secondarily on price and

total formulation costs. To a lesser extent, GTL base oils

will also compete with Group II+ in a growing market for

5W-30. Rather than reducing the value of GTL by moving

down the quality continuum to Group I and II base oils,

GTL base oils are expected to park themselves in the

high-end market space of Group II+, III, and IV and be the

beneficiaries of specification pushed demand into its

space. This will occur by increasingly stringent

performance requirements and market acceptance of 5W- and

most importantly 0W-xx PCMO.

In

addition to GTL competing in the emerging low viscosity

passenger car motor oils markets, it will also penetrate

automotive driveline applications, premium diesel engine

oils, high-end industrial lubricant applications, and

white oil applications over the next five to eight years.

Adoption of GTL base oils is expected to occur at a faster

rate in Europe than in the US due to the rate of market

acceptance of 0W-xx engine oils. In addition, GTL will

penetrate the Asian market.

Copyright © Petroleum

Trends International, Inc. 2002

|