|

The

True Value of the

Lubricant

Additives Business

Compoundings

Magazine, March 2002

By

Thomas F. Glenn

Petroleum

Trends International, Inc.

The

lubricant additives business is big, complex, and a key

part of the lubricants industry. In addition, it’s a

changing business and one that adds significantly more

than chemical packages and components to the value

chain. It is also a business well positioned to add even

greater value in the future. Understanding this value

and how it might evolve starts with a look at the

position additive suppliers have in the value chain.

Links

in the Chain…

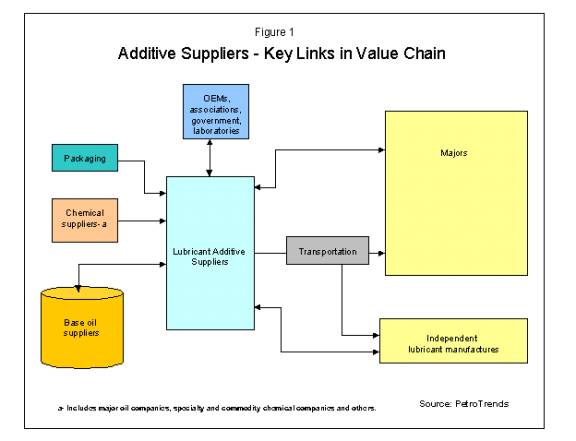

Lubricant

additive suppliers are an integral part of the

lubricants value chain. They connect with seven major

links in the chain, as shown in Figure 1, and play a key

role in defining and refining the functionality of

finished lubricants.

On

the buy side of the chain, additive manufacturers

purchase base oils to solubilize additives, and dilute

them into manageable concentration. Collectively,

consumption of base oil by additive manufactuers in the

US reached close to 130 million gallons in 2001 and

includes both paraffinic and napthenic. In addition to

purchasing base oils, additive manufacturers also work

collaboratively with base oil manufacturers to optimize

performance in new stocks.

Another

link on the buy side of the value chain for additive

manufacturers are suppliers basic in

such intermediate chemicals as amines, dodecyl

phenol, olefin copolymer, methacrylate,

styrene-isoprene, and other raw materials used to

manufacture lubricant additives. Although some lubricant

additive manufactures are basic in these and other

chemistries, the diversity of materials required to

manufacture additives necessitates the need for most to

purchase some raw materials from other suppliers. In

addition to adding value to these materials by milling,

reacting, compounding, and packaging for use as

lubricant additives, additive manufacturers also add

value by leveraging buying power, assuring consistent

quality, and by working with raw material suppliers to

enhance performance.

Packaging

manufactures represent another buy side link in the

value chain. Although a significant quality of additive

is shipped in bulk, additives are also sold in 55-gal

drums and other containers.

The additive manufacture’s link to packaging

material suppliers can also go beyond buying. It

sometimes includes interactions regarding issues related

to the compatibility of finished lubricants with

packaging materials, appearance, and other

considerations.

Another

critical link in the value chain is the highly

interactive one additive manufactures have with original

equipment manufacturers (OEMs), trade associations,

engine test laboratories, government agencies and others

involved in influencing, implementing and assessing the

performance of lubricants. Additive suppliers work

collaboratively with these stakeholders to develop

specifications and test protocols, assure compliance,

establish timetables, provide information, and to

address health and safety and other product and

application related issues.

The

sell side of the value chain for lubricant additive

manufactures includes primarily major oil companies and

independent lubricant manufacturers. Taken together,

additive packages and components purchases by majors and

independent in the US reached and estimated 2 billion

pounds value at almost $1.6 billion in 2001. These

numbers alone, however, do not speak to the true value

of the business or its potential moving forward.

The

true value of the business…

Rather

than competing simply as suppliers of chemicals,

lubricant additive manufactures have evolved into a role

where they are highly competent, collaborative, and

proactive partners with virtually all stakeholders in

lubricant value chain. They are expected to work with

these stakeholders to develop and meet the continuously

changing performance requirements of all finished

lubricants. They are also expected to work with

customers to develop proprietary formulations, address

blending issues, build on market intelligence, position

products, solve problems, and handle technical and

customer service related issues. As a result, expertise

and technology in both product development and additive

manufacturing have become the core competency of most

lubricant additive manufactures. And for most, these

competencies are a requirement of being in the additives

business, not an option. This reality, together with the

bandwidth additive suppliers have in the value chain,

electronic interconnectivity of lubricant industry stake

holders, redundancies in the value chain, the industry

life cycle, intensity of competition, and others suggest

that additive suppliers are well positioned to

contribute even more to the lubricant value chain in the

future… This

will be the subject of the next Top Line column.

Copyright © Petroleum Trends International, Inc. 2002

|